"No Tax on Tips" Zelle Trap: Why Your Clients Might Miss the Deduction

Let’s keep the conversation going on "No Tax on Tips," because this is where we have to shift from just tax preparation to true tax advisory.

We now have Notice 2025-69, and it gave us a very important clarification that changes everything for gig workers and service professionals: Only tips that are included on Form 1099-NEC, 1099-MISC, or 1099-K count toward the tip deduction.

This matters. A lot.

I have shared this story during our sessions, but here is the long version. Settle in.

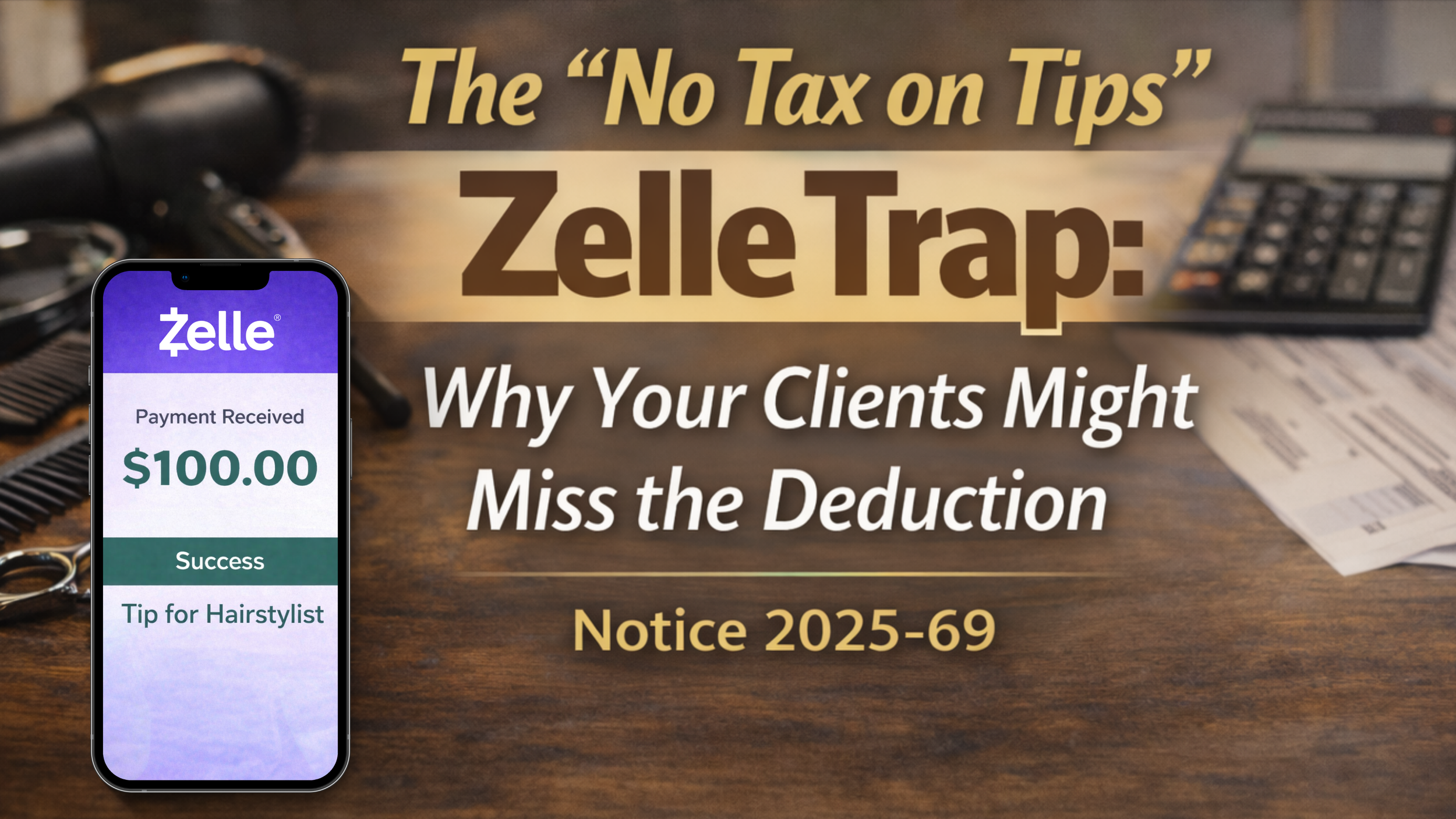

The Hairstylist, The App, and The "Perfect" Plan

I have always paid my hairstylist through Zelle. We both liked it because it avoids credit card processing fees. It is simple, clean, and cheaper for her.

Back in May, when the talk of “no tax on tips” was circulating but before anything officially passed, I told her the good news. She was excited. Every client tips. Trust me, business owners know exactly which clients do not tip.

Then the law passed.

Section 224 stated the requirements for qualified tips, and from what I read, she checked every box:

Customary Industry: The industry must be one that has customarily received tips prior to 2025. (Very common for hairstylists.)

Method of Payment: Tips received from customers, paid in cash or charged. (I pay her via Zelle.)

Voluntary Nature: Tips must be voluntary. (I even tipped extra when she straightened my hair instead of my usual blow dry.)

The Cap: Deduction capped at $25,000. (She easily gets tipped by most clients; for the year she has received close to this amount.)

Not an SSTB: Not be a Specified Service Trade or Business.

Filing Status: If married, must file Married Filing Jointly.

ID Requirements: Valid Social Security number authorized for work.

At that point, everything looked good.

Then Came the Fine Print (Notice 2025-69)

Section 224(g) gave the Treasury Secretary authority to establish additional requirements for what counts as qualified tips.

Well, the Treasury Secretary on November 21, 2025, issued Notice 2025-69 where they stated:

Tips received by non-employees only qualify if they are included in amounts reported on Form 1099-NEC, 1099-MISC, or 1099-K. (See bottom of page 16, top of page 17 in the Notice).

Here is the problem: Zelle is not a third-party settlement organization (TPSO). It is a bank-to-bank transfer.

That means:

No Form 1099-K

No automatic reporting of those tips on an official 1099

No way for those tips to qualify for the deduction under the notice

Right before Christmas, I had to break the news to her. The very payments we thought were “smart” from a fee perspective were now disqualifying her from a tax deduction.

Advisory Moment: Change the Business Process or Not?

This is where you come in as a tax advisor. The conversation is not just: “Switch to only accepting credit cards.”

The real conversation involves asking the deeper questions:

What is her effective tax rate?

How much tip income do you typically get in a year? Is it close to $25,000, or much less?

What is the actual tax savings from the deduction?

How much would she pay in credit card processing fees?

Is the return on investment there?

For some clients, the answer will be yes. For others, absolutely not. That will be a decision your client makes, but as advisors, we are there to help them understand the requirements and estimate the tax savings, or reveal there might not be savings at all.

And that is exactly why this is not a quick-answer tax prep issue. This is advisory work.

Keep leaning into these conversations. This is where the real impact (and real value) is found.

We learn together. Grow together. Succeed together.

Join the Inner Circle

Are you navigating these sticky advisory moments with your clients? Join the Nadia CPA Inner Circle where we dissect notices like 2025-69 and build the strategies you need to lead your clients with confidence.